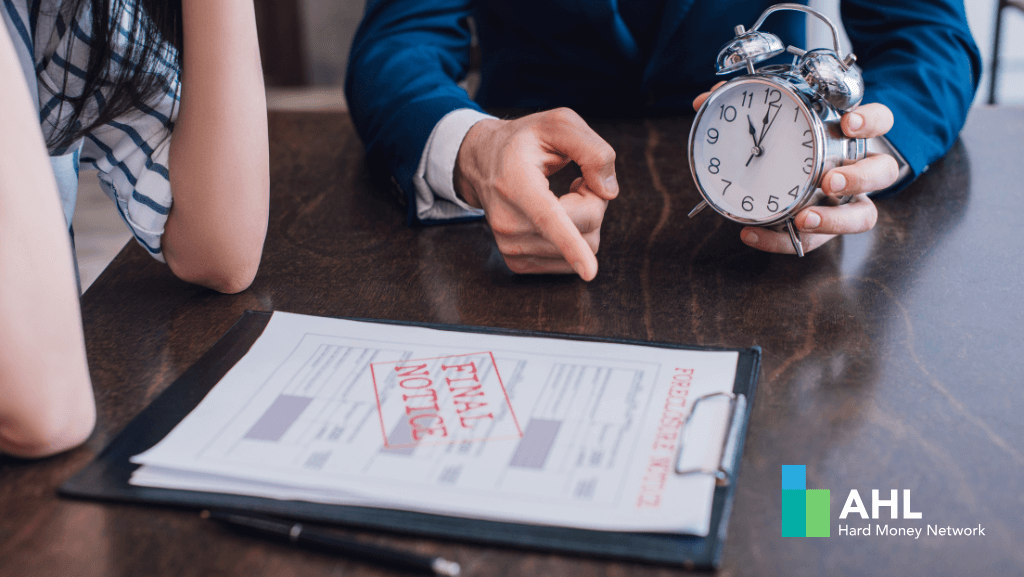

Facing foreclosure in Florida can be an incredibly stressful and daunting experience. The threat of losing your home can feel overwhelming, but it's crucial to remember that you have options and resources available to help you navigate this challenging time. This blog post will outline key resources for Florida homeowners facing foreclosure and explore a specific solution that might be a lifeline: a private money loan refinance.

The moment you receive a notice of default or see the signs of financial distress, it's time to act. Ignoring the problem will only worsen the situation. Here are some crucial initial steps:

Florida offers a variety of resources designed to help homeowners avoid foreclosure. Here's a breakdown of where to find assistance:

These agencies provide free or very low-cost counseling services. A HUD-approved counselor can:

You can find a HUD-approved housing counselor near you by:

Organizations like InCharge Debt Solutions offer free and confidential financial counseling to help you review your income, expenses, and debts, and explore options to avoid foreclosure.

When traditional lenders or government programs aren't an option, or when time is of the essence, a private money loan refinance (also known as a hard money loan) can be a viable solution to stop a Florida foreclosure.

A private money loan is a short-term loan secured by real property, typically issued by individuals or private companies rather than traditional banks. For homeowners facing foreclosure, a private money loan refinance means obtaining a new loan that pays off your existing mortgage, effectively stopping the foreclosure process.

While a private money loan can be a lifesaver, it's essential to be aware of the following:

A private money loan refinance is often considered a "loan of last resort" or a strategic bridge loan. It's best suited for Florida homeowners who:

Facing foreclosure is a challenging situation, but with the right information and resources, you can explore every avenue to protect your home. A private money loan refinance can be a powerful tool in your bailout strategy, offering speed and flexibility when you need it most.

© 2025 AHL Hard Money Loans - All Rights Reserved | Privacy Policy | Website by DigiSphere Marketing